10 pay whole life insurance is a straight forward product. An insured/policy holder makes 10 payments to the contract and after that the policy is guaranteed paid up forever and always. Not surprisingly a given level of death benefit for a 10 pay whole life product will have a considerably higher required premium than a whole life policy that requires premium payments for a longer period of time (say to age 100).

The product is well known for its generally higher rate of return for both cash value and death benefit given premium vs. other whole life products, but the market for 10 pay whole life insurance is pretty thin. Luckily, however, a few common participating whole life insurance players entered the 10 pay market this year and we’ve been waiting for an opportunity to compare their products and we figured there’s no better way to do that than to round up performance among most everyone in the market at the moment.

First, let’s start with a little word of caution. This comparison is a serious deviation from our typical discussion as it relates to cash value life insurance. We’re generally known for talking—at length—about the manipulation of a permanent life insurance policy’s reserve to generate substantial cash values in the policy for asset growth and/or retirement income generation.

Today, on the other hand, we’re going old school. No blending no paid-up additions and instead just plain whole vanilla whole life insurance paid up easily in 10 years.

We looked at four different scenarios and we calculated internal rate of return (aka Compound Annual Growth Rate) of the the cash value and death benefit given our planned premium in each scenario so that we could compare performance of the policies.

Our evaluated policies were for a male age 35 standard risk with a $25,000 annual premium, a female age 35 standard risk with a $25,000 annual premium, a male age 55 standard risk with a $25,000 annual premium, and a female age 55 standard risk with a $25,000 annual premium.

While we could have specified a death benefit and calculated return given the premium (whatever they figured out to be in each case) we chose this approach because it’s infinitely easier—and oh so much quicker—when don’t have to plug in a bunch of different premium values to calculate rate of return.

We calculated rate of return for years 10, 20, and 30 for both the given cash surrender value of the policy and the death benefit of the policy. All values used for the calculation are assumed values and not guaranteed values.

The companies that we looked at for this analysis were: The Guardian, MassMutual, MetLife, Ohio National, and Saving Bank Life of Massachusetts (SBLI). Whenever a carrier would not allow a policy to be issued to a proposed insured based on age we simply dropped them from the comparison (e.g. some carriers would not allow their policy to be issued to a 55 year old insured).

We wanted to include New York Life because while they might not have a bona-fide 10 pay whole life product, their customer whole life product will allow for a dialed in 10 pay whole life scenario. Unfortunately, however, their software was being extremely temperamental and we had to leave them out (maybe later we’ll attempt to update this and add them if certain other companies decide to enter this space).

The newcomers to the 10 pay space are MetLife, Ohio National and SBLI. All three companies rolled out 10 pay whole life products just this year, and we’ve been excited to see how these would compete against the old 10 pay mainstays Guardian and MassMutual (two companies whose products have been near or at the top of our lists for life insurance as an asset class designs often times with their 10 pay products).

This was our chance to compare these new policies against each other, and against the current establishment. The results were somewhat shocking, and in other respects pretty much what we expected.

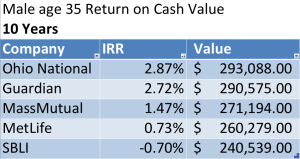

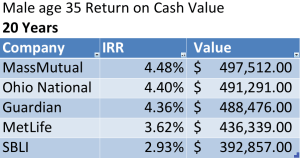

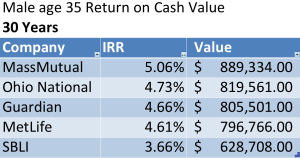

First up are the numbers for the 35-year-old male on cash value and death benefit. On the cash value side Ohio National shot to the top of the list by year 10 followed pretty closely by Guardian. The two were overtaken, however, by MassMutual come year 20—by a small margin and then a much more significant on come year 30.

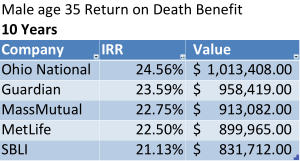

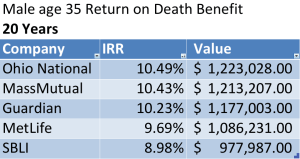

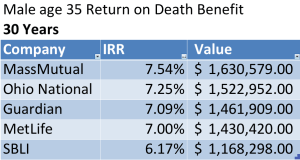

For death benefit it’s was more of the same. Ohio National led in year 10 followed closely by Guardian, and Ohio National held on to a marginal lead over MassMutual in year 20. But again MassMutual jumped to a pretty large lead by year 30 over the rest.

MetLife and SBLI held onto consistency, placing forth and fifth in all years respectively.

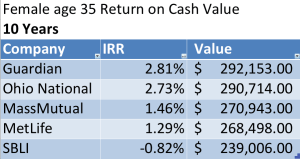

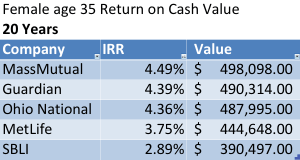

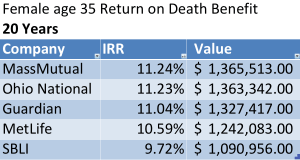

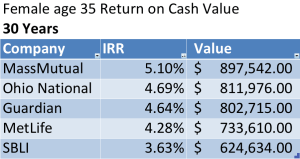

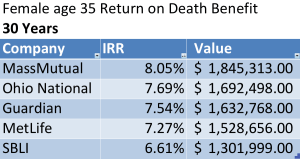

Now on to our 35-year-old female.

Cash value wise, Guardian started out as the leader somewhat narrowly over Ohio National in year 10, but was narrowly beaten by MassMutual come year 20 and by year 30 MassMutual again performs significantly above the rest. MetLife and SBLI continue their consistent placing.

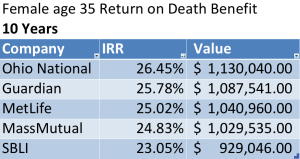

For death benefit Ohio National starts out in the lead, and yet again MassMutual slips by in year 20 and runs away by year 30. MetLife and SBLI continue to hang out at the bottom of the list.

We weren’t surprised to see MassMutual perform as well as it did. We were a little surprised to see Guardian fall behind Ohio National to the degree that it did, though we’ve known Ohio National to perform pretty well cash surrender value wise compared to competition in the past.

There was no real shock to MetLife’s cash value and death benefit performance here. They’ve been pretty well known for a very generous long term dividend assumption that will help income generation (not evaluated in here) but their cash surrender value tends not to win favors.

SBLI’s performance was somewhat interesting. This new 10 pay from SBLI is a very different beast from the company’s old product—known for it’s positive cash value in year one. The No Nonsense Company ® junked that product around the first of this year in favor of a less idiosyncratic policy. The old product was well known for its very high very early cash surrender value, but also well known for its severely lagging cash surrender values longer term. The assumption was that if they dropped the high performing early cash value, they’d compete better in the longer term, but that’s doesn’t appear to be the case from this comparison.

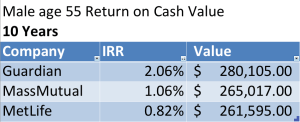

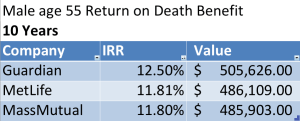

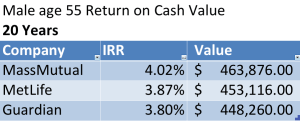

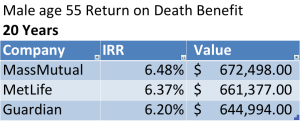

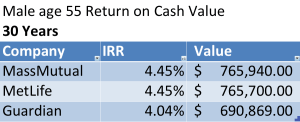

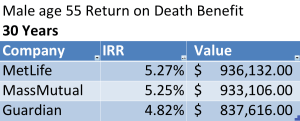

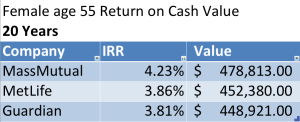

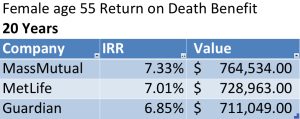

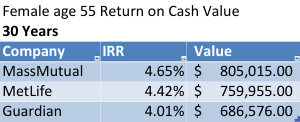

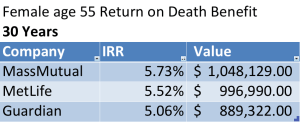

Since Ohio National and SBLI don’t allow an insured who is 55 to purchase their 10 pay products, we had to leave them out, leaving us with Guardian, MassMutual, and MetLife. Results were very noteworthy

For the male age 55 cash surrender value started with Guardian in the lead by year 20 both MassMutual and MetLife has jumped over Guardian and by year 30 MassMutual and MetLife projected values that were statistically the same (in fact we’ve never seen a scenario where two carriers projected values so close to one another).

Death Benefit wise, Guardian again started strong, but fell behind both MassMutual and MetLife by year 20. By year 30 MetLife took the top spot for return.

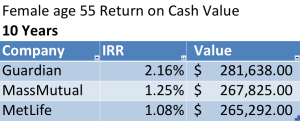

For our female age 55 on the cash value side Guardian again starts strong with MassMutual and MetLife jumping over by year 20, this time however MassMutual maintains a pretty strong lead over MetLife even by year 30.

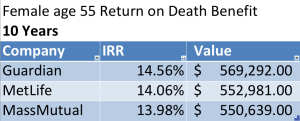

And on the death benefit side Guardian starts out placing first by year 10, with MassMutual and MetLife overtaking in year 20 and again MassMutual maintains a stronger lead in this scenario when it comes to year 30.

We’re pretty impressed with MetLife on this one. Beating out Guardian in several years evaluated, and rivaling MassMutual for the top spot in the male scenario was quite an impressive feat. The long-standing rumor that Snoopy likes older insured’s seemed to be validated by the results here.

We have to tip our hat to MassMutual on this one. Mass placed first in more years than anyone else, and the wide availability of the product is certainly very appreciated. Not to mention MassMutual has a solid track record for very consistent performance.

We’re also very impressed with the performances pulled off by Ohio National and MetLife. Being newcomers to this scene and doing as well as they did means we’re pretty sure someone at their respective Home Offices is well versed in building competitive products, and we like the idea of that.

This isn’t a call for everyone to run out and buy MassMutual’s 10 pay whole life product. The evaluation here was merely to look at what carrier products performed the best for cash value and death benefit given a pretty narrow scenario. It’s a starting point, not an ending point.

If cash surrender value is really the focus, there are other ways to accomplish this (and we’d strongly argue a better way), and if one were looking to maximize return on premium dollars for death benefit, we’d have to bring endowed guaranteed universal life insurance into the mix to fairly assess just how well that situation is handled with any of these carriers.

And that’s the round-up for basic 10 pay whole life insurance.